NEWS ANALYSIS: "1,300 African startup jobs gone in 90 days. What founders should do right now."

Good News: Africa's Fintech Era Is Over.

For years, fintech led the story building the rails through payments, wallets, and digital banking. Now the capital is moving into logistics, energy, and mobility. Not because fintech failed. Because it worked. What we’re seeing now is a shift from building financial rails to building real economy infrastructure on top of them. Companies like Spiro, GoCab, and SolarAfrica are not competing with fintech. They are extending it. This is what ecosystem maturity looks like. The question is no longer where the fintech money went. It’s what fintech has made possible.

The Anatomy of an Investor Deck

8 Metrics Every Startup Founder Should Track

Innovation Hubs in Africa: What Have They Actually Produced?

The Anatomy of a Pitch Deck: What Investors Are Actually Looking For

What Is Product–Market Fit? PayPal’s Reentry into Nigeria Case Study

Africa’s Readiness for UN’s 2030 Agenda (A Founder & Systems Lens)

The Four Stories Every Founder Must Tell Before Asking for Buy In

Foresight Africa 2026: What the Brookings Report Really Means for African Founders

Decoding the Matrix: How African Founders and Investors Can Redesign Economic Freedom - My AfroTalks

The Cost of the Wrong Capital Game: How Ami Colé Won the Market but Lost the Business

From Hustle to Infrastructure: How African Unicorns Are Redefining Everyday Systems

This shift from hustle I also refer to as the ‘IRT factor’ to infrastructure signals the next chapter of Africa’s digital transformation. We have singled out these four companies, showing exactly how that evolution is playing out.

5 Tips for Investors in African Tech Markets

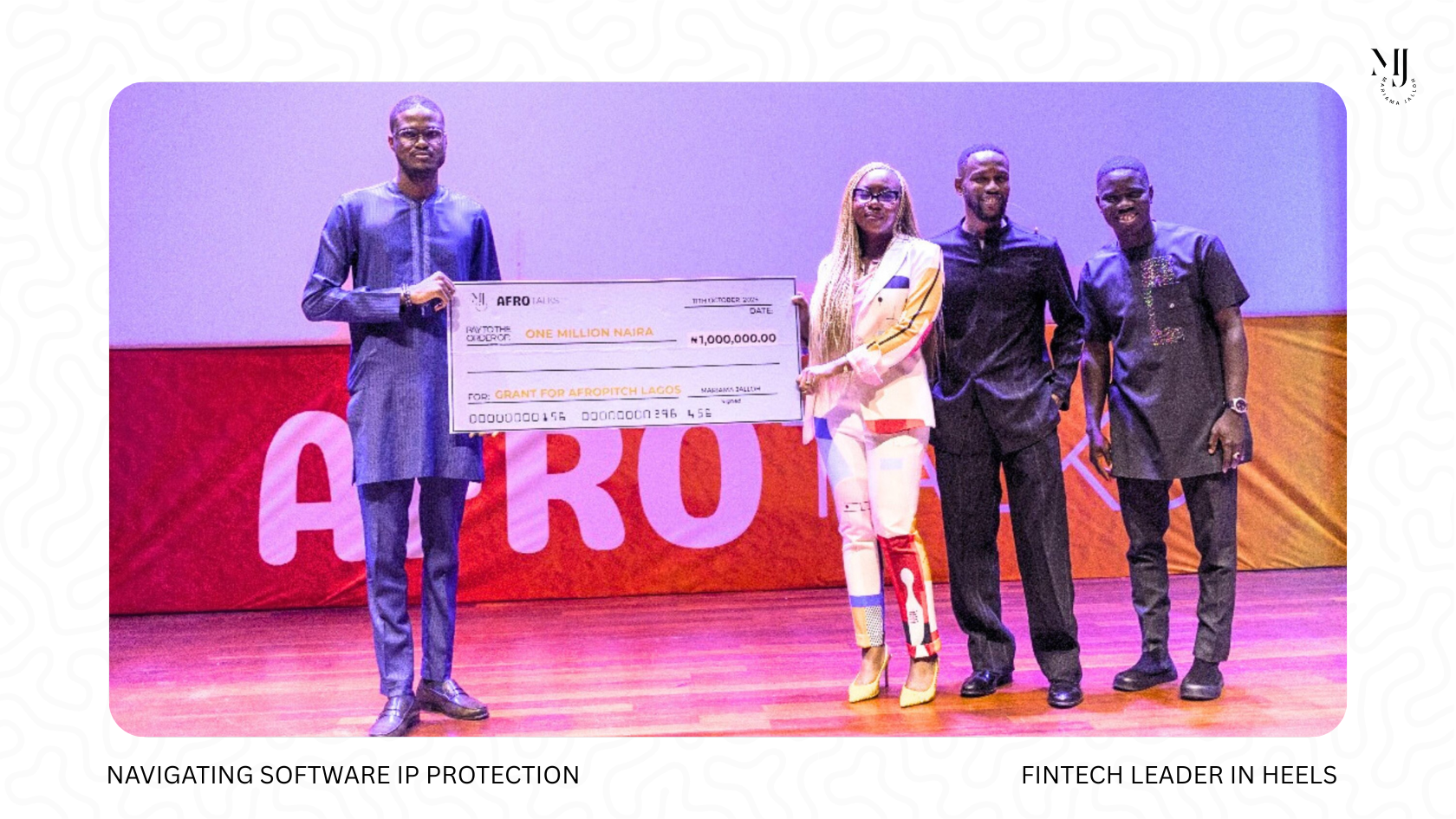

Uncharted Territory: Navigating Software IP Protection Across Africa’s Diverse Markets

Reducing ECOWAS Travel Costs: Lessons from the EU for Africa’s Free Movement Vision

Cross-Border Fintech Licensing: Can Africa Build Its Own ‘Fintech Passport’?

The IRT Factor: Why Ingenuity, Resilience, and Tenacity Define Founders in Emerging Markets

Across Africa, Latin America, and South Asia, founders aren’t building inside predictable systems they’re building in spite of them. And the entrepreneurs who thrive are powered by what I call The IRT Factor: Ingenuity. Resilience. Tenacity.

AI Is Transforming Industries but Is Africa Ready?

In Lagos, Accra, and Nairobi, homegrown machine learning labs are tackling real-world problems verifying identity without credit histories, predicting crop yields with satellite data, or creating AI-powered translation tools for indigenous languages.